Mini Chapter Eight

How Greeks adapt to smiles

- Sticky Strike model/rule does not change the implied vol for any of the strikes i.e. the vol is sticky to the strike irrespective of the movement in the underlying. Mathematically this would imply = 0 (this would be better understood as you read on), and hence the portfolio’s delta to equal Black Scholes delta. For equity markets that typically have a downside/negative skew, move higher in the underlying index would lead to the progressive ATM strikes to lose implied vol. Or seen another way, an equity dealer who models ATM vol cheaper as markets rally, also expects the stock buying/exuberance to continue. On the contrary applying this on EM FX vol curves that typically have a topside/positive skew, a move up higher in spot (weaker EM FX) would mean progressively expensive ATM vol. Either way dealers for both asset classes expect future implied vols across strikes to be aligned with the current implied vol curve.

- Sticky Delta model/rule values options with a conservative/moderate outlook on volatility by keeping the implied vol unchanged across deltas i.e. as the underlying moves and changes the moneyness for every strike, the implied vol adjusts to align with its delta. As an example if we have purchased a 25 delta option at inception, in case of a move in spot which aligns it with the strike (i.e. it’s now an ATM option) it would need to be revalued using the implied vol of the ATM strike at inception. In other words the rule maintains the same implied vol for ATM delta (suggesting no strong longer term directional bias for the underlying’s volatility) and vols for the other strikes adjust to their changing delta, moving the skew in the direction of the underlying. This rule is more suitable for trending markets with again no change in realised vol.

- Impact of Skew on Delta Hedging (Smile Delta) – by now we understand well the existence of an implied vol (IV) surface and the pricing models of dealers that can have subtle differences from each other. Every strike on an open option position for a dealer would have a model-generated IV taking into account a skew to reflect both market levels and dealers’ bias for their risk. Refer to the graph on Call Deltas for instance with changing implied vols – out of the money strikes have higher deltas as vols are marked higher while in the money strikes have lower deltas. The reverse is true for lower vols. The delta that’s hedged after adjusting for this volatility skew is called the Smile Delta. A sanity check on end of day vol levels is therefore important to hedge the right deltas.

- Adapted Delta – for the sake of completeness this is another name for smile delta, with its name suggesting how delta adapts to the changing implied vol (of the option’s strike) as the underlying spot moves. Following from above there is either an addition or erosion to the Black Scholes Delta by this adaption amount (that assumes no change in vol) depending on the vol surface.

-

- Consider the different types of smiles below:

-

- Flat smile - same as Black Scholes assumption of flat vol across strikes hence irrespective of spot move, = 0 and 𝚫Adaptive = 𝚫Black Scholes

- Symmetrical smile (higher wings and low/no skew)

- Let us consider a Long Call option with ATM strike which is the lowest point of the smile (Implied vol curve). For a move up in spot the strike will roll up on the downside wings thus IV will increase. This makes d𝛔/dS positive in the adapted delta notation and thus 𝚫Adaptive > 𝚫Black Scholes

-

-

-

- Conversely if Spot moves down and the Strike moves up on the upside wings it gains on implied vol and is negative, hence 𝚫Adaptive < 𝚫Black Scholes

-

-

-

-

-

- In the money and out of the money scenarios are also covered in the table below

-

-

| Initial Strike | Spot ↑ | Spot ↓ |

|---|---|---|

| At the money | Positive | Negative |

| In the money | Positive | Positive |

| Out of the money | Negative | Negative |

- While the example above is that of a call, if we were to replace it with a put the signs for in and out of the money strikes would get flipped. Effectively it’s the placement of the strike (whether left or right to the ATM) that decides the signs of d𝛔/dS in response to the movement in spot.

- Note that the multiplicative effect of Vega would be a function of strike placement too i.e. it would maximum at/around the ATM and lower for deep in/out of the money strikes. The adaption effect on account of vega therefore diminishes with strikes on the wings.

Skewed smile

That could either exhibit a skew (higher implied vols) for lower strikes namely ‘downside skew’ or for higher strikes namely ‘upside skew’. Important to consider strike placement again to assess the direction of movement in implied vol as the spot goes up or down. Risk reversals (RR, with strikes typically out of the money) are best examples to illustrate the impact of spot movement on a strike’s implied vol. But importantly when the economics of an ATM, butterfly and risk reversals are combined the shape of the smile curve is better defined (more on this later). For now, consider a downside RR where d𝛔/dS is always positive because:

- Move up in spot would shift the existing ATM on to the skew and downside strike further up the on the skewed left wing to attain a higher implied vol

- While a move down in spot would shift the existing ATM towards the right and the downside strike down the skewed left wing to reduce its implied vol

| Risk Reversal | Spot ↑ | Spot ↓ | Adaption effect |

|---|---|---|---|

| Topside | Negative | Negative | 𝚫Adaptive 𝚫BS |

| Downside | Positive | Positive | 𝚫Adaptive 𝚫BS |

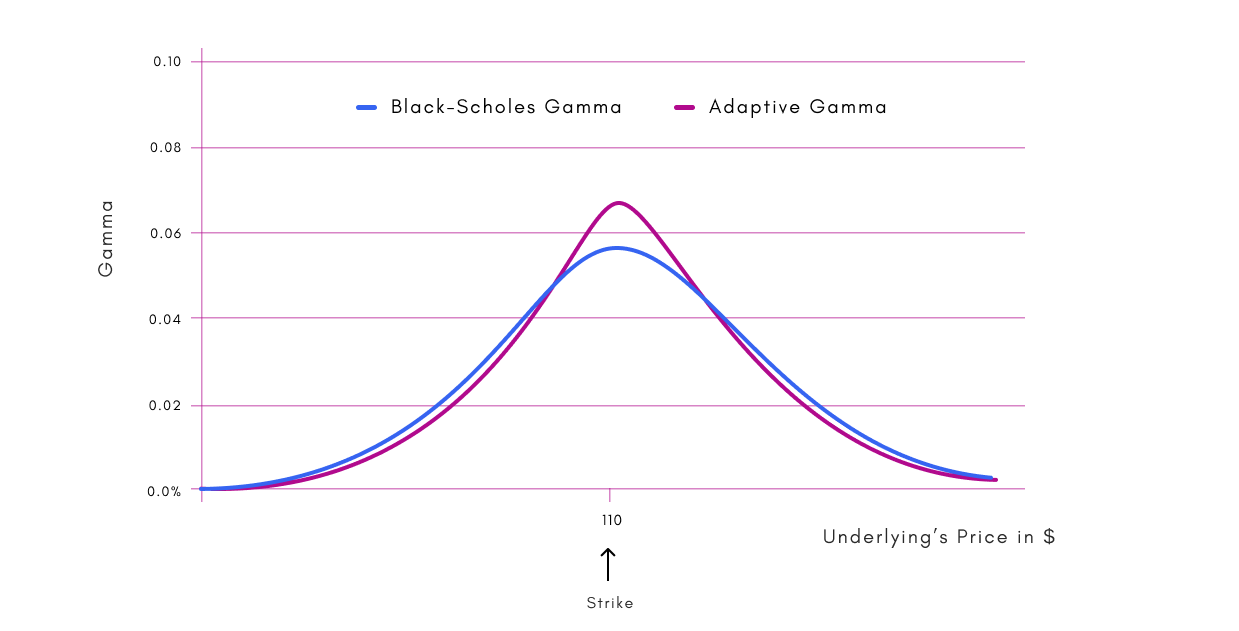

Adaptive Gamma

After adapted delta, this smoothly follows now i.e. the adaption effect is the difference between Adapted gamma and Black Scholes Gamma. Being the rate of change of delta if you consider:

- A vol smile with steep wings and low/no skew as discussed above would exhibit a definite move in implied vol and hence the adapted delta (vs black scholes delta) for both an up/down move in spot. This implies high (positive) gamma around ATM strike, that also intuitively makes sense as alongside a high vega at/around ATM the curvature both sides also picks up on the IV smile with a movement in spot. As strike moves away from ATM, it loses vega and hence the drop/rise in adapted delta vs black scholes delta is lesser; adapted gamma for more in/out of the money strikes would be below black scholes gamma.

Graph 16 – Black Scholes vs Adaptive Gamma in case of low/no skew

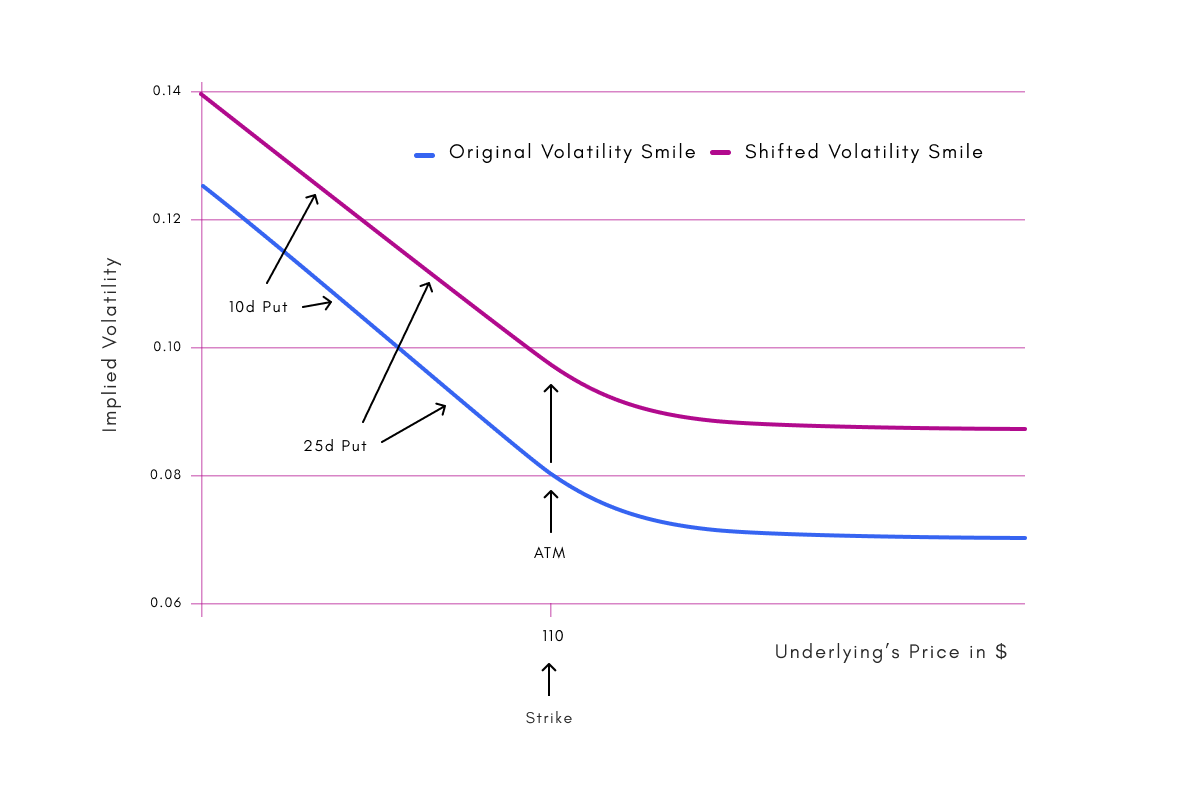

Adaptive Vega

Last of the greeks to consider for adaption is the change in the price of the option as implied vol changes i.e. Vega. This is best reflected by assessing the change in the implied vol smile as implied vol for the ATM strike is nudged higher. Refer to chart xx on a long call option delta profile at different implied vols – delta profile stretches out at higher IVs i.e. strikes to the left of ATM gain delta and while strikes to the right of ATM lose delta for higher implied vols. The vol smile therefore stretches out as ATM implied vol is nudged higher and the strikes on the higher wing of the smile gain less vol versus those on the lower wing. In other words:

- for strikes on higher wing of the smile, Vega Adapted < Vega Black Scholes

- and for strikes on lower wing of the smile, Vega Adapted > Vega Black Scholes

Graph 18 – ATM Vol shock to a smile with a downside skew

Source: Pandemonium.