Mini Chapter Fourteen

Risk Reversal

- Risk reversals involve trading out-of-money calls vs out-of-money puts (usually both calls and puts have similar percentage delta at inception). In the real world, different strikes of an underlying usually have different implied vols unlike what Black Scholes suggests. Hence, this strategy is a directional view on the vol skew on different strikes of the underlying asset. Buying of a risk reversal would mean buying the skew i.e. (usually) buying the higher vol vs selling the lower one.

- For a topside RR, the uncapped upside one buys is financed by selling the uncapped downside or vice versa. And so while the total delta of the option at inception is twice that of a call or a put (assuming both calls and puts have same percentage deltas), the options are generally traded with delta-exchange as the view is mainly on the vol skew and not so much on the starting delta.

- The vol skew also determines the strikes for a specific delta. Higher the implied vol (IV) of a certain OTM strike, other things equal, the further away it is from ATM. Similarly for lower IVs, same delta strikes move closer to ATM.

- To further elaborate on the skew – if we are long an OTM Call and short an OTM put – as the underlying rallies we would be gaining gamma and vega. Very often, ATM vols for certain underlyings have a distinct correlation with its spot movements. E.g. Implied Vols for USDCNH FX go up when spot moves higher and comes off when spot falls. In such a case it is advantageous to be Long a topside Risk-Reversal (RR) on USDCNH as the vega profile of the option would deliver positive/increased vega as spot levels go up at a time when implied vols are moving higher. On the other hand, if spot were to come off, one would get negative vega but that would usually correspond with lower implied vols with falling spot and hence would be cheaper to vega-hedge.

- Connecting the Dots

There’s a fair bit of reference to steep forward curves especially for EM currencies and while this observation may not be useful to experienced practitioners, I thought of including it nonetheless in case it helps those starting out. Being long the EM currency/short dollars on a steep forward is akin to being long carry all else being constant. Drawing a parallel with the options world – being long an OTM USD put vs EM call would earn carry with no change in underlying spot i.e. outright forwards roll down towards spot and the out of the money strike moves closer to ATMF over time and gain delta/go up in value.

- For USD/EM, we observe that pricing of topside options is almost always skewed higher versus downside options (Implied vols for OTM Calls are higher than Implied Vols for OTM Puts). Similarly in an underlying like S&P Index it is generally observed that downside options are more expensive than upside options again due to hedging demand as well as due to the increase in volatility during market crashes as compared to during bull periods. This pricing differential of Implied in 25D Calls vs 25D Puts (Risk Reversal) is also termed as vol skew and can be seen across the vol curve.

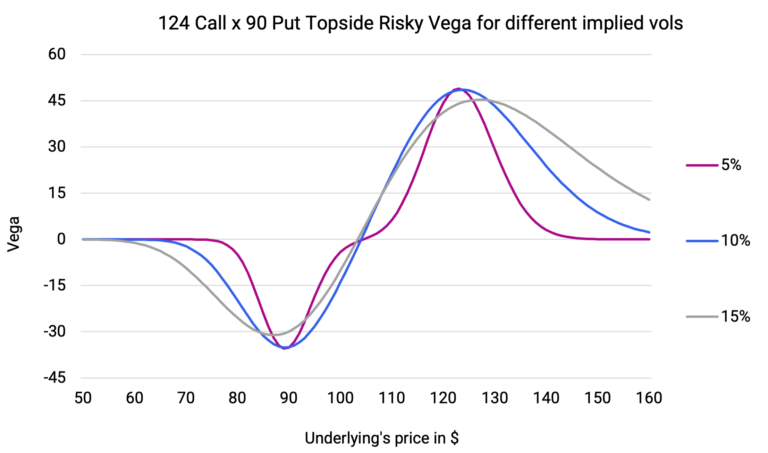

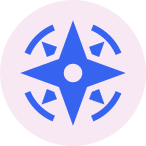

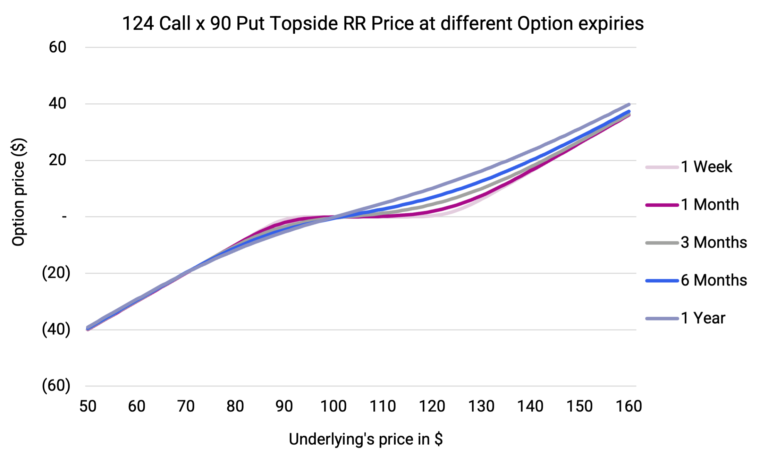

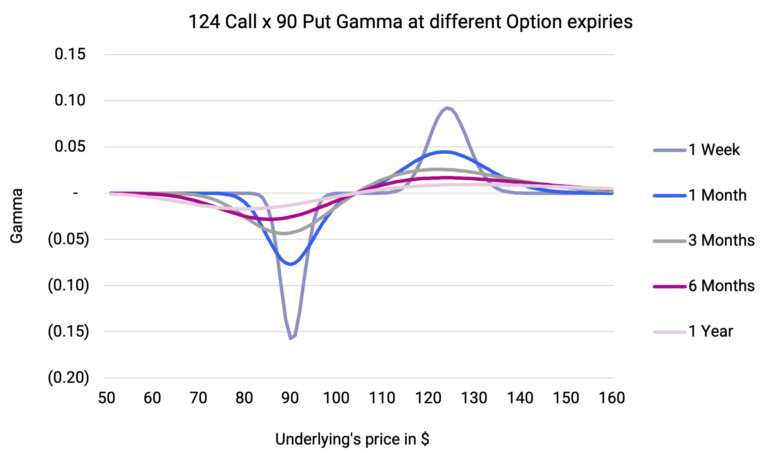

- Consider the graphical representation of a ~25 Delta Topside Risk Reversal for an equity stock on different option expiries with a 5% skew (IV for Call 5% above IV for Put). Notice that this strategy is largely a play on Vanna i.e. the change in Risky’s vega due to change in spot, or the change in option’s price sensitivity to the change in implied vol.

Graph 53 – Topside Risky prices across Option expiries

Graph 54 – Topside Risky Delta across Option expiries

Graph 55 – Topside Risky Gamma across Option expiries

Graph 56 – Topside Risky Vega across Implied Vols