Mini Chapter Four

Put-Call Parity

Put-Call Parity – is a key zero-arbitrage concept in the European options world which explains that the total payoff of taking opposite directions on a put and a call option on the same underlying at the same strike price (even if different from the current market price) is the same as the payoff of either going long or short a forward contract on the underlying at that strike price. Hence the difference between the premium on the call and a put is equal to the difference between market price and the discounted value of the strike. Consider the below:

- Pc = call option premium, Pp = put option premium, B = current market price, X = strike price, present value has continuous discounting at the risk free rate = Xe-rt

- Long Call and Short put at strike X can be entered by paying (Pc – Pp)

- At any time in the option tenor up to maturity, payoff on this strategy would be B – Xe-rt (note at maturity t = 0)

- Payoff on a long outright forward position at strike X at any time during and upto the maturity of the position would be exactly the same.

- The zero arbitrage on the above return profiles is the basis of Put Call Parity denoted by the following equation: Pc – Pp = B – Xe-rt

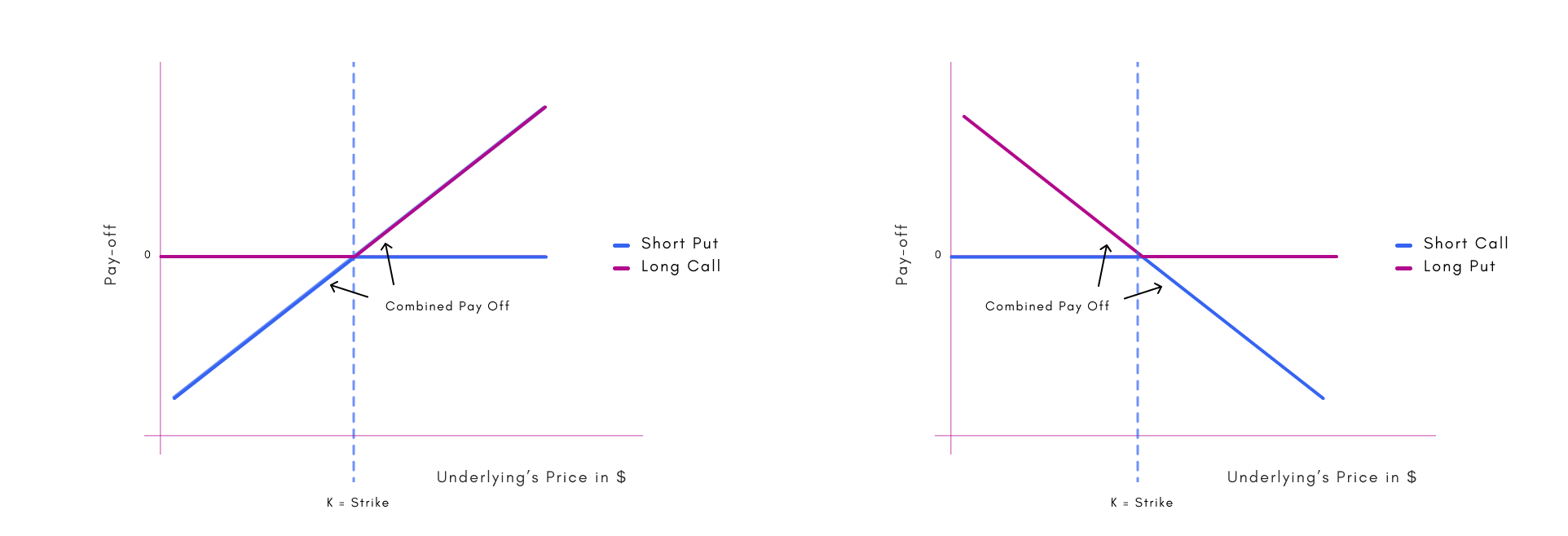

Graph 7 – Payoff diagram – cover both scenarios of long/short Call vs Short/long Put

Source: Pandemonium.

- As a follow-up to the above one can rearrange the equation and conclude for instance that the value of a portfolio composed of LHS should equal the value of a portfolio composed of RHS:

-

- Long Call option + Long Strike = Long underlying at current market price + Long Put

-

- Also as a corollary if the strike chosen (i.e. present value of the forward price discounted at r) is the same as the current market price, then the price of call is the same as the price of put.